Zillow Removes Vital Climate Risk Info on Real Estate Listings

| . Posted in News - 0 Comments

By Eric Weld, MassLandlords, Inc.

When Zillow, the nation’s leading online real estate marketing platform, recently removed climate change-related risk data from its property listings, it robbed prospective buyers of a valuable resource in determining their new property’s worth and future liability.

Without the climate-related risk data that Zillow recently removed from its property listings, many homebuyers may find themselves dealing with flooded and under-insured homes. Homebuyers, especially younger people, are increasingly factoring weather-related risks into their investment decisions. (Image: flickr CC0 Public Domain)

For about a year and two months, from September 2024 to November 2025, Zillow had posted helpful climate change-related risk factors on its property listings. Using data generated by the First Street Foundation, which has become the industry leader in researching and predicting climate change risks, Zillow posted risk factor ratings for flood, fire, wind, air quality and heat on its property ads.

If you were shopping Zillow for property during that window, you would have seen statistics about the likelihood of a given property suffering certain weather outcomes at certain points in the future. A box on the ad would include a rating such as “Severe 8/10” for flood factor, for example. It might have advised that “Flood insurance is critical” for a property, and given both historical flood data and future statistical projections of the property’s likelihood of flooding in the next year, next 15 years and next 30 years.

This is information any real estate buyer would want to know. As the earth’s overall temperature continues to rise, flood risk in particular is increasing in Massachusetts due to heavier rainfall and storm surges, as well as rising sea levels’ risks to coastal properties.

Wildfires, on the rise along with flooding, are the second foremost concern among homebuyers factoring climate-related risk into their property investment decisions. Zillow removed weather-related risk ratings from its property listings that could assist homebuyers in making smart investment choices for a warming planet. (Image: cc by-sa Wikimedia commons Jeff Turner.)

Why Did Zillow Start Listing Risk Data?

Zillow began listing weather-related risk data in an attempt to be transparent and forthright about a property’s future liability due to climate change weather risks. Homebuyers, especially younger people, are increasingly factoring potential weather risks into their location and purchasing decisions.

Zillow found, in a 2023 study, that more than 80% of prospective homebuyers consider climate risks. Most of those respondents specifically listed flood risk as their chief concern, followed by wildfires. Both those risks have increased with climate change.

“Climate risks are now a critical factor in home-buying decisions,” noted Skylar Olsen, Zillow’s chief economist, in a 2024 announcement by Zillow Group of the new policy to list risk factors on property ads. “Healthy markets are ones where buyers and sellers have access to all relevant data for their decisions. As concerns about flooding, extreme temperatures and wildfires grow – and what that might mean for future insurance costs – this tool also helps agents inform their clients in discussing climate risk, insurance and long-term affordability.”

We opened Zillow, entered a Massachusetts town at random and looked at the first listing it showed us. This listing was for a single-family home with two bathrooms. At time of writing, there was no climate score data visible. (Image License: Fair use)

Why Did Zillow Stop Listing Risk Data?

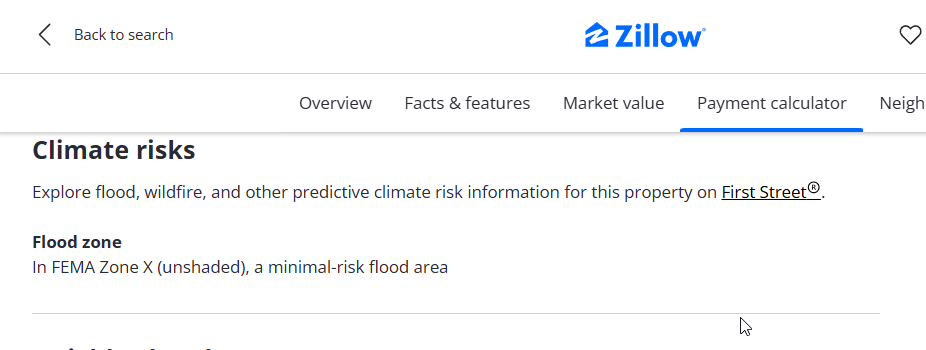

Despite the logical reason for starting its policy to list flood and other climate risk data on property listings, Zillow abruptly changed its policy in November 2025, pulling the data from its listings. In place of data, Zillow now provides a link to First Street Foundation under the heading “Climate risks,” after scrolling deep into a listing. “Explore flood, wildfire, and other predictive climate risks for this property on First Street,” prompts the link.

First Street’s homepage invites you to search any address in the U.S. and provides a readout of flood, fire, wind, air quality and heat ratings for that property.

Below the link on Zillow’s listings is also a flood zone rating from FEMA, based on the agency’s national flood maps, and whether a given property is low, moderate, high, undetermined or coastal high risk.

Zillow’s decision to discontinue prominently listing First Street flood and other climate change risk data on its listings was apparently based on economy, and data uncertainty. When the California Regional Multiple Listing Service (CRMLS) and other real estate industry groups and some home sellers complained that the risk data was negatively impacting housing prices, and in some cases wasn’t accurate, Zillow changed its listing policy.

The policy reversal may seem unfair to home shoppers and prospective buyers. Imagine purchasing a rental property unaware that it’s located in a high-risk flood zone, only to find out later that you can’t procure flood insurance because of the high risk. Or worse, when spring melting arrives your new property is flooded repeatedly due to high water tables.

Of course, home buyers should dig deep into the data of a property they want to invest in, where they can still access climate change risk data. But many real estate shoppers won’t see or click through to the First Street statistics, and crucial weather-related data will remain a mystery even as they go through the purchase process. Real estate agents are unlikely to volunteer such information and jeopardize shaving the asking price due to weather risk.

Practical economy superseded fairness in Zillow’s decision.

Questionable Data?

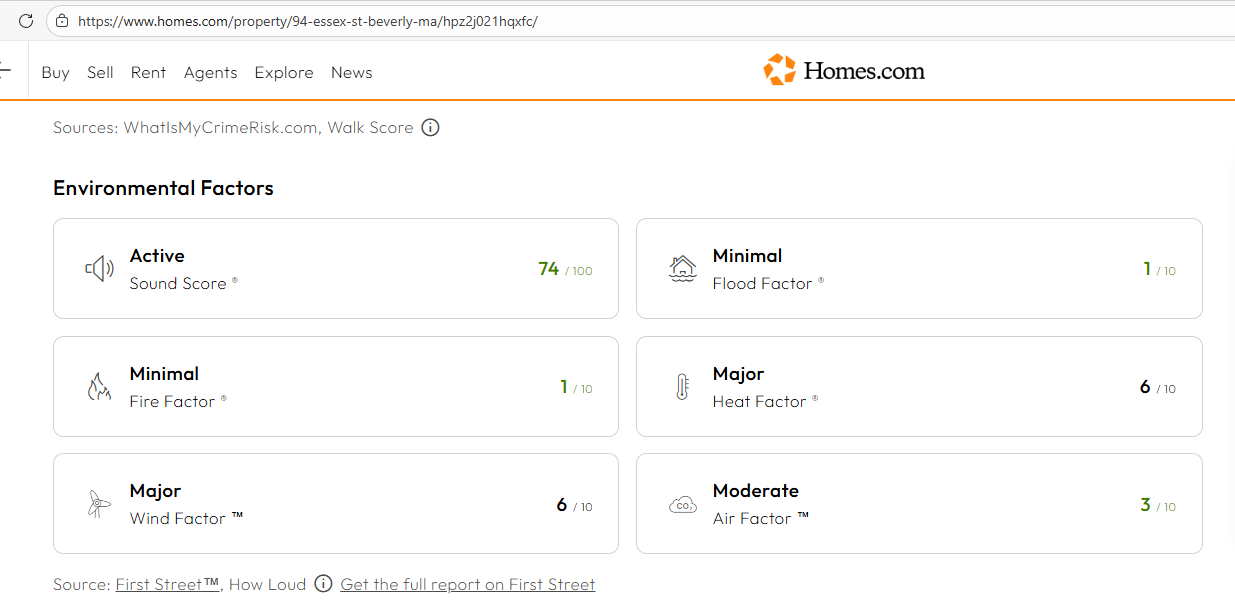

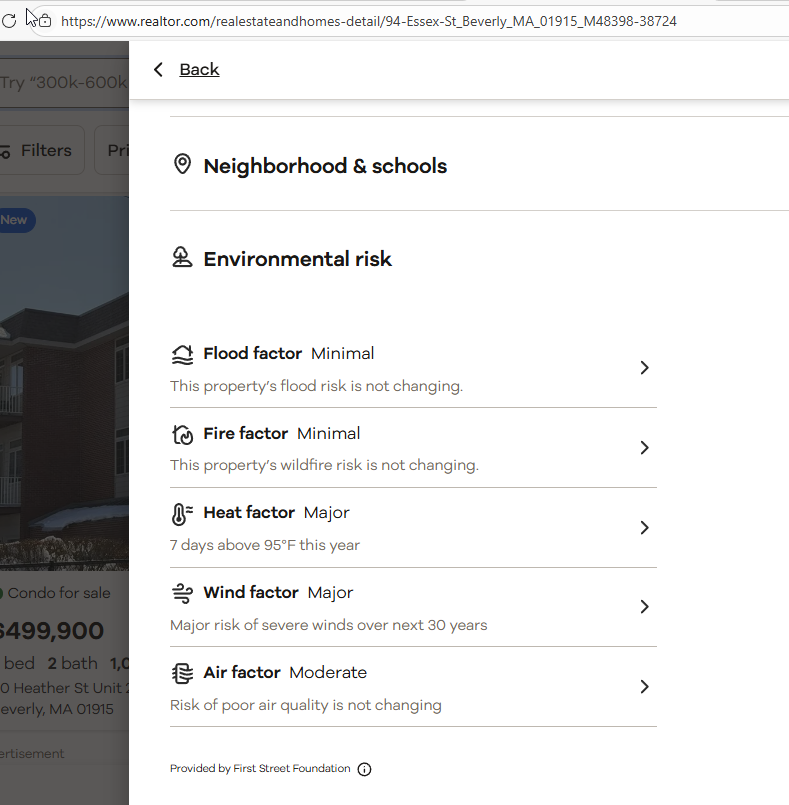

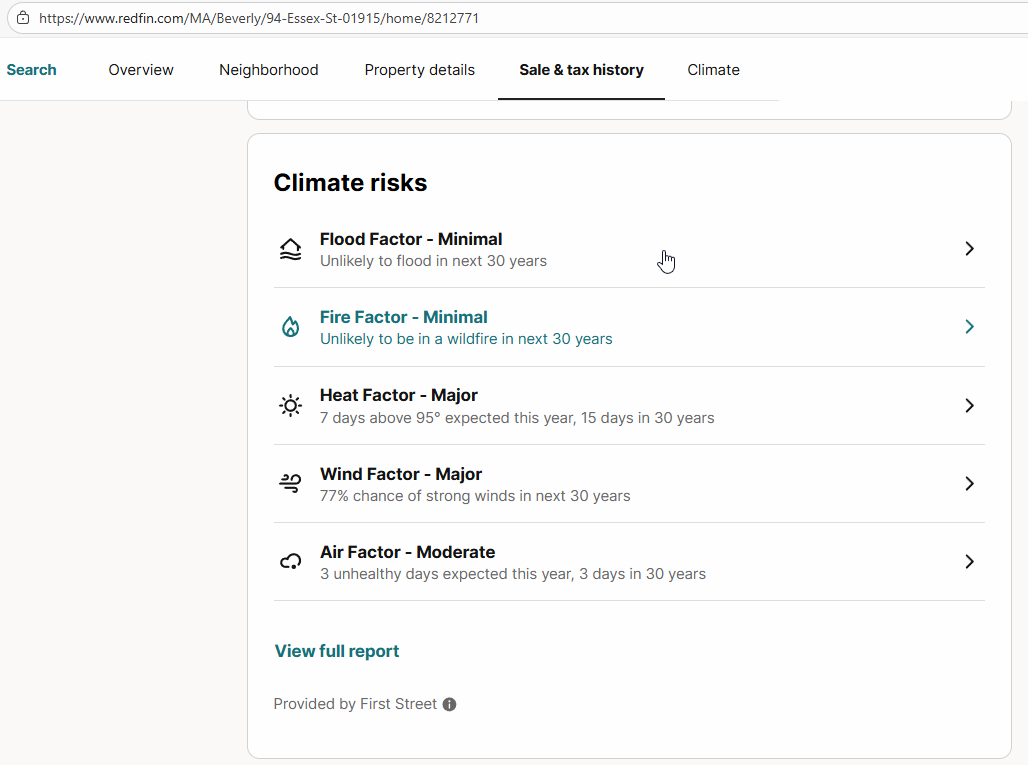

Though Zillow has pulled risk data from its listings, other real estate platforms, such as Homes.com, Redfin and Realtor.com, continue to list specific “Environmental risk” (Realtor.com), “Climate risks” (Redfin) or “Environmental factors” (Homes.com) on their property listings, also culling from First Street data.

As of time of writing, Homes.com still showed First Street risk metrics for fire, wind, flood and heat for the random property we sampled. (Image License: Fair use)

In its lobbying to Zillow to pull climate change risk data from its listings, the CRMLS and others also complained that the data was and is often generalized, inaccurate and not geared specifically enough to individual properties. Some home sellers balked about the flood ratings of their properties, noting large, inexplicable discrepancies compared to other properties on the same street, for example.

As of time of writing, Realtor.com still showed First Street risk metrics for fire, wind, flood and heat for the random property we sampled. (Image License: Fair use)

Moreover, home sellers said they were frustrated that because First Street data is based on future projections, it’s too easily accepted and not considered refutable. And while Redfin and Realtor.com allowed a process in which individual customers could have weather risk data removed from their listings, Zillow did not allow such removal.

As of time of writing, Redfin.com still showed First Street risk metrics for fire, wind, flood and heat for the random property we sampled. (Image License: Fair use)

First Street argues that its data models are based on scientifically validated, proven, peer-reviewed methodologies. The organization posts its methodologies on its website for all to see.

Madison Condon, an associate professor at Boston University School of Law and an expert on climate change, financial risk and regulation, points out that the First Street data models may be helpful for certain uses. “With forward-looking models, we can’t check their outputs against a record, they are necessarily forecasting events that have not yet happened,” she said in a New York Times article about the Zillow risk listings. “But what level of accuracy is good enough changes substantially if the question is about one specific property you are about to spend your life savings on.”

First Street Chief Executive Matthew Eby countered those charges by pointing out that his organization’s transparent data models have been validated by major banks, federal agencies, insurers and engineering firms.

Climate Blind Home Shopping

It makes sense that home buyers, especially younger people, are factoring climate-related risks into their purchasing decisions. Still, despite well-documented flood and wildfire risks to properties in particular areas, such as along coasts and in dry, windy areas, people continue buying and living in properties in climate risky areas.

For now, Zillow remains a leading online real estate platform. That means, for millions of people shopping there, climate risk data may not be a suitable component in their home purchases. That will lead to a lot of surprises when new homeowners or multifamily investors learn they can’t insure against flooding, or have to deal with flooding itself.

As it is, several insurance companies have stopped or reduced coverage for homeowners in California due to the prohibitive cost and high possibility of natural disasters there, mostly from wildfires. National agencies like State Farm, Allstate, Nationwide and Farmers Insurance Group have stopped accepting or reduced new property insurance customers from California.

Zillow has made a market-based decision not to directly provide climate-related risk factors for home shoppers on their website. But the issue certainly is not going away as carbon increases in our atmosphere, storm severity increases and flooding and wildfires continue to increase in frequency and intensity.

Perhaps Zillow will reverse its reversal at some point and assist its customers again in making wiser decisions that include climate risks to their homes. Meanwhile, we advise home and rental investors to use more forthright platforms like Homes.com, Redfin and Realtor.com, where climate-related risks are enumerated on each property listing.